Now, this is no Greece for two reasons:

- Greece defaulted because it couldn't afford to pay its bills as borrowing rates soared across the board to unbelievable heights. Meanwhile, the US is still at historic lows for borrowing rates, even in the face of a threat of the debt ceiling.

- If the US defaults, it was a selective default because Republicans artificially presumed the need for slashed spending in the face of low borrowing rates. The day after Republicans stop being stupid and agree to raise the ceiling and quit using the economy as a bargaining chip, is the day both the markets and the US government resumes normal operations.

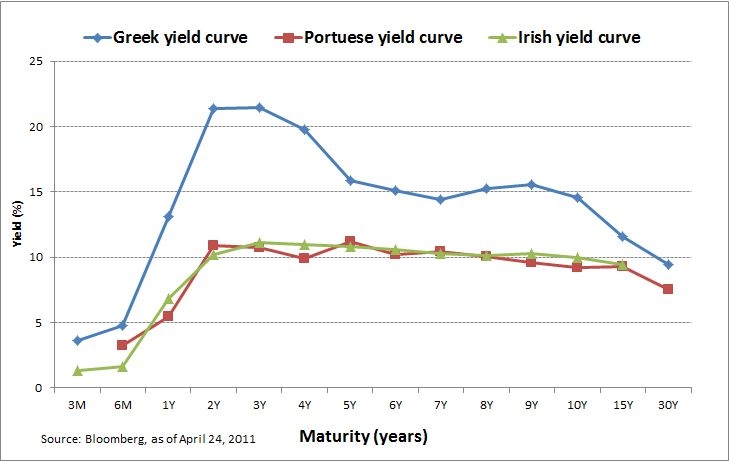

We're a long ways away from having the sort of yield inversion that Greece exhibited. Still, it's worth paying attention that the markets are now expecting Republicans to hold their ground and keep the debt ceiling in place.

No comments:

Post a Comment